Sole proprietorships, partnerships, family businesses … each bring with them both challenges and opportunities that can impact your financial security. Ensuring that you set your business up for success from the beginning can mean the difference to your bottom line. For planning, consideration, and guidance many professionals have entrusted Rutwind Brar to identify the right solution for their business that is a custom fit.

We can help you identify the advantages and opportunities that exist through:

- Incorporation

- Sole proprietorship

- Holding companies

- Share structure

- Income splitting, and even

- Payroll set up

Is your business account closely integrated to your family finances? We can help you to ensure that your family business provides for the financial security of yourself and your loved ones both now and into the future. Whether your focus is on financial security or simply to save where possible on your annual taxes, at Rutwind Brar, we can help you establish a structure for best results. Contact Us today to explore your options as you establish your company’s structure.

Blog posts about Structuring Your Business

The new financial year is almost here, and a new budget along with tax changes for businesses and individuals has already been introduced. In order to begin with your tax preparation for the new financial year, you must be aware of the changes in personal taxes made by the Minister of Finance and the Canada Revenue Agency (CRA).

Bill Morneau, the Minister of Finance, announced a new budget on February 27, 2018 (Budget 2018). The budget had some tax changes for businesses owners and individuals. To know what are the changes in personal taxes, let us first take a look at the existing personal tax. Here are the Federal Personal Income Tax Brackets and Tax Rates for the financial year 2017-2018.

- 15% on the first $45,916 of taxable income, +

- 20.5% on the next $45,915 of taxable income (on the portion of taxable income over $45,916 up to $91,831), +

- 26% on the next $50,522 of taxable income (on the portion of taxable income over $91,831 up to $142,353), +

- 29% on the next $60,447 of taxable income (on the portion of taxable income over $142,353 up to $202,800), +

- 33% of taxable income over $202,800.

According to the new budget, the federal tax rates are unchanged, but the brackets have been changed by an indexation factor of 1.015. The indexation factors, tax brackets, and tax rates have been confirmed by the Canada Revenue Agency (CRA). The new federal tax rates for 2018-2019 are as follows:

- 15% on the first $46,605 of taxable income, +

- 20.5% on the next $46,603 of taxable income (on the portion of taxable income over 46,605 up to $93,208), +

- 26% on the next $51,281 of taxable income (on the portion of taxable income over $93,208 up to $144,489), +

- 29% on the next $61,353 of taxable income (on the portion of taxable income over 144,489 up to $205,842), +

- 33% of taxable income over $205,842.

Your federal tax rate is based on your income. The federal tax is the portion of your taxable income before any credits and benefits. Apart from paying the taxable amount to the Canada Revenue Agency, a specified percentage has to be paid to your province too. This additional amount is known as the provincial income tax.

Here are the provincial taxes for Alberta for the financial year 2017-18.

- 10% on the income up to $126,625, +

- 12% on income between $126,625.01 and $151,950, +

- 13% on income between $151,950.01 and $202,600, +

- 14% on income between $202,600.01 and $303,900, +

- 15% on income over $303,900.01

According to the changes suggested, the provincial tax brackets and tax rates for the province of Alberta look as follows:

- 10% on the first $128,145 of taxable income, +

- 12% on the next $25,628, +

- 13% on the next $51,258, +

- 14% on the next $102,516, +

- 15% on the amount over $307,547

Some Additional Information Regarding New Tax Changes and Payments:

- Self-employed individuals have until June 15, 2018, to file their return.

- From February 26 to April 30, 2018, the CRA will be offering extended evening and weekend hours for Individual Tax Enquiries. The lines will be open from Monday to Friday (except holidays) from 9:00 am to 9:00 pm (local time) weekdays, and from 9:00 am to 5:00 pm (local time) on Saturdays.

Source: https://www.canada.ca

In order to ease the process of filing your personal tax returns, you can hire an accounting firm. Get in touch with us, and we will help you gain the right tax benefits and ensure you file the correct tax amount.

Are you managing your accounting and bookkeeping on your own because you haven’t found the right accountant in your city? Or are you doing it because your in-house resources are unable to manage the constant pressure of bookkeeping? Whether you don’t have a trusted accountant in your city or your in-house staff are not knowledgeable in bookkeeping and accounting, virtual accounting services can be an ideal solution for you.

Virtual accounting services are the usual accounting, bookkeeping, and financial services remotely provided online by a team of accountants, or ‘virtual accountants.’ Let us explain some of the top benefits of virtual accounting services.

Less Paperwork, More Productivity

When you have an in-house accountant or bookkeeper who doesn’t use the proper accounting software and/or applications, your office can be flooded with lots of paperwork. Keeping track of paperwork and maintaining physical books can be challenging and time-consuming. But, when it comes to virtual accounting services, virtual accountants maintain and update every detail of your records within one type of software and provide a dashboard for you to access. This means no paperwork at your workplace and more productivity thanks to the online resources.

Timely Access to Accounts

As a business owner, you might want to take a look at your financial statements and reports at any hour of the day. Another benefit of virtual accounting services is that you can access your financial statements 24/7 from any part of the world. When you have an in-house accountant taking care of your accounts, you have to ask for your account statements and wait to receive them. But when it comes to virtual accounting services, they will provide all the reports and statements you need on a daily basis, so the information that will help you run your business is right at your fingertips.

Low Cost

When you opt for virtual accounting services, you can save yourself a significant amount every year. If you have an in-house accountant, you will have to pay them a salary, bear their sick leave pay, payroll taxes, recruitment costs, employee benefits, etc. But when it comes to virtual accounting services, you will receive a package of varied accounting, budgeting, and bookkeeping services at affordable prices. Unlike physical accountants, you can avail these virtual services for 365 days a year without paying extra.

Flexible Hiring

Virtual accounting services can be hired on a need-basis. There are months when your accounting and bookkeeping needs will be higher. For instance, when you want to file your tax returns, you will need your accountant the most to calculate the taxable amount and pay the taxes on time. Similarly, there may be months when you won’t need an accountant. If your accounting and bookkeeping needs are low, then you can opt for part-time virtual accounting services. This way, you not only save on the cost of hiring a full-time in-house accountant, but also on the full contract of virtual accountants.

Virtual accounting service providers are a team of accountants who use secured software to get the job done for you. Companies that hire virtual accounting services have been more successful at growing their business, increasing revenue and reducing cost. So, then if you are considering virtual accounting services for your business, then get in touch with Rutwind Brar.

Managing your finances and books of account can be a tedious task when you run a business. It is all the more difficult when you lack the basic knowledge of accounting. The solution is to hand over the work to a chartered professional accountant. A chartered professional accountant is a member of a profession which was created in Canada after an amalgamation of three professions, Certified General Accountant (CGA), Chartered Accountant (CA) and Certified Management Accountant (CMA). A chartered professional accountant is a professional who handles important accounting and income tax related issues and works on advising and consulting businesses to make better financial decisions. To give you a picture of what a chartered professional accountant does, here are some key benefits of hiring a chartered professional accountant.

Comprehensive Accounting Knowledge

Whether you have a large, mid-sized or small business, maintaining your accounting books is essential. Trying to do it on your own may seem feasible to you but could be a bad decision if you lack the extensive knowledge required to do so. When you hire chartered professional accountants, they bring with them their knowledge and expertise in accounting. The combined nature of their job role helps you with your bookkeeping, tax management, and business advisory as well.

Better Decision Making

As mentioned before, the extended job role of a chartered professional accountant makes them a highly knowledgeable person when it comes to accounting. Their knowledge can come in handy for your business as a chartered professional accountant will be able to help you with financial planning and decisions based on your firm’s current position.

Detailed Expertise in Taxation

For any business owner, the major discrepancies that happen in their accounting system are because of the lack of accounting and tax knowledge. The problem is not the lack of willingness to pay the tax but the lack of awareness about tax laws, rules, deductions, required tax returns, and deadlines. Having a chartered professional accountant to guide you fills up this gap of unawareness and ensures that you do not fall behind on your tax filings. They also help you claim deductions which you may have not even heard of, thereby saving your money.

Varied Services

A chartered professional accountant is a comprehensive profession which works on the varied accounting services which a business requires. When you choose to hire an internal accountant, he comes with the knowledge of one person. But when you hire a chartered professional accountant from a good accounting firm, their knowledge and services are not limited to just one person, and you get access to the varied services they provide which will prove helpful for your business.

When we talk about the smooth functioning of a business, we plan to run it successfully. With your finances and accounts managed by a chartered professional accountant, you have an updated statement of your accounts. Also, having someone to take care of your accounts enables you to work on other business related responsibilities. So let the professionals work on your accounts while you work on your business.

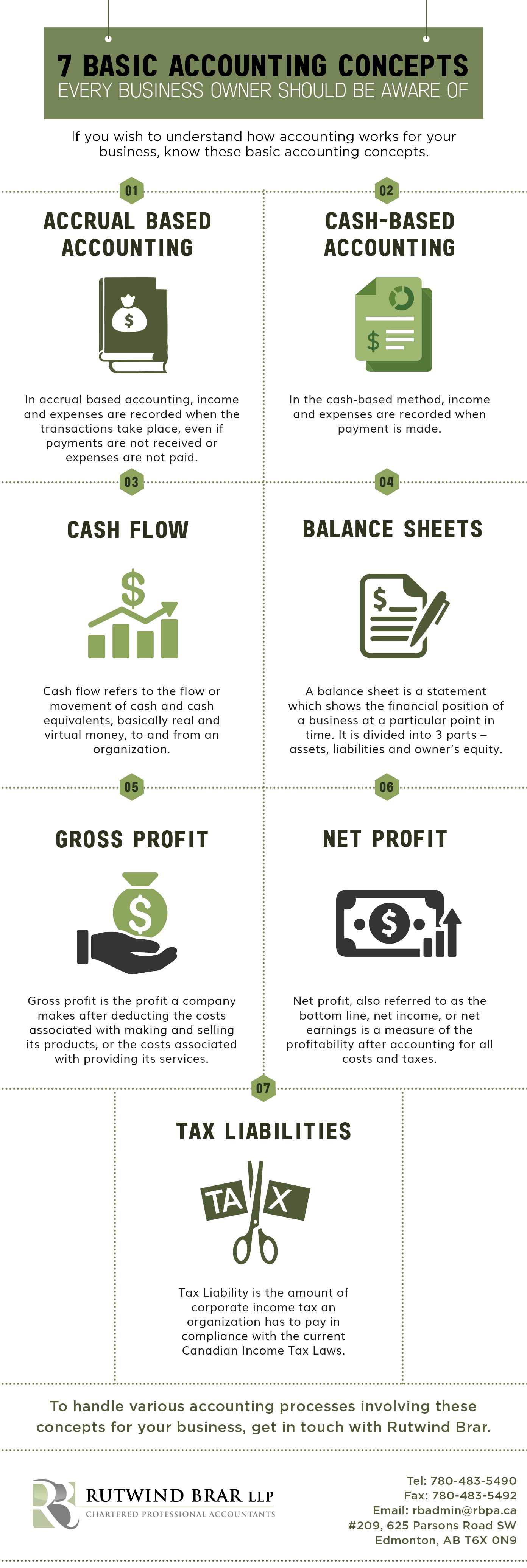

When we talk about the basics of accounting, we often hear that accounting is all about managing your assets and liabilities. This happens because assets and liabilities are the most common terms which everybody is familiar with. But their familiarity with these terms is limited. People without the base background of accounting do not understand what assets and liabilities exactly are. So what are assets and liabilities?

An Edmonton accountant will describe assets as the materials, property, and resources which hold monetary value and belong to an entity. Assets can be tangible or intangible. Tangible assets are things which can be seen and touched such as building, home, vehicles, machinery, etc. Intangible assets are resources which are not visible or touchable such as copyrights, trademarks, patents, etc.

A liability as per Edmonton accountant is a debt or obligation that a company owes to someone, which is required to be paid up in monetary or non-monetary forms. Common examples of liabilities include accounts payable, salary and wages payable, taxes, debts, etc.

Types of Assets

1) Fixed Assets

Fixed assets refer to the assets which are owned by the business and used to generate income. The business does not plan to sell them in the short run but plans to keep them and use them for years. Common examples include office premises, commercial vehicles, machinery, etc.

2) Current Assets

Current assets are short-term assets of the business which are a part of the business for a brief period. These assets remain in the business for not more than one year or so as these assets get used up within a short period. Common examples include short-term investments, stocks, cash, and inventory, etc.

Types of Liabilities

1) Current Liabilities

Current liabilities are dues and debts that the business needs to clear within a one year. This will include your accounts payable or credit suppliers who have provided you with raw materials for the business on credit basis. It will also include the excess money if any withdrawn from the bank as an overdraft. Other examples include tax liability, interest payment, etc.

2) Long-term Liabilities

Certain debts and obligations need not be fulfilled at the earliest or within a year. These are known as long-term liabilities. Mortgages, bank loans, business- issued bonds are some common types of long-term liabilities.

To sum it up for you, assets and liabilities are what you own and what you owe respectively in your business. Having the knowledge about the same is necessary as it helps you finalize your accounts properly. If you still have doubts about assets and liabilities and find it difficult to maintain your books of accounts, then you need to hire an expert Edmonton accountant.

Do you analyze your business accounts and your accounts receivable from time to time? If yes, then sometimes, you might have come across overdue or pending invoices. You might surely have some clients who don’t pay on time creating potential cash shortfalls and stress. Getting your payments from some customers on time can be a little tricky if they follow the same pattern every time you issue invoices to them. The challenge of getting your clients to pay in a timely manner can be managed easily. Here are some helpful tips suggested by accountants in Edmonton that will help you deal with your overdue accounts receivable.

Explain Your Terms and Expectations

It is important to explain your company’s invoicing and billing policies and expectations to your new debtors to avoid any confusion or disputes later. Be clear as to your company’s payment policy. For instance, most businesses offer a 30-day payment policy. Also, mention to your clients that if they fail to pay within your payment duration, you will charge interest on the payable amount. Furthermore, mention all other crucial invoicing terms that you have for your clients.

Follow Up and Send Reminders

Follow up with your clients after the service has been provided, the products have been delivered, or the project has been completed. Remind them on a regular basis during your payment grace period. You can either send gentle reminder messages, emails or official reminder letters. Don’t overdo or become too pushy while following up and sending reminders. Repeated follow-ups might irritate your clients. And most important, do not get angry or irritated, or don’t threaten them while following up. Doing so will only spoil your corporate relationships.

Appoint a Staff Member

You might have several things to do as a manager or business owner. Therefore, assign one of your employees or hire an accountant specifically to follow up with your clients, send reminders, and collect payments from them. This will save you a lot of time and energy that you can invest in other important tasks. You will always have one point-of-contact in charge of your accounts receivable.

Offer Discounts and Levy Penalties

For timely clearance of invoices, you can set-up an upfront or an advance payment policy. Offer discounts to clients who make payments within a short span and levy penalties or interests on late payments. Ensure your clients are aware of these policies as this will be an incentive for your clients to make early payments and save money.

You will always have different experiences with various clients. Some clients will generally clear their invoices reasonably quickly while others may continue to take their own time to clear the invoices. In any scenario, accountants in Edmonton suggest business owners to stay calm and try to manage their overdue invoices by following the tips mentioned above.

Companies that sell products (and not services) have a financial reporting requirement called Cost of Goods Sold (COGS). Also referred to as “Cost of Sales”, COGS is an important term used in corporate accounting. It is a measure of the total direct costs incurred in producing goods that are purchased by customers. The sole purpose of calculating COGS is to compute the true cost of producing the merchandise that consumers purchased over the year. There are quite a few prerequisites to know what COGS is and how is it calculated:

1. What Does COGS Include?

COGS includes only those costs which are directly related to the manufacturing of the product. This can encompass the cost of raw materials used, labour to produce the product, items bought for resale and production overhead charges. For example, the COGS for an automobile manufacturer would include the material costs incurred in developing the car parts and the labour costs needed to assemble the car. It would not include the shipment charges, general administrative expenses or the labour put in to manufacture and sell the car. Further, COGS will not consider the costs for those cars which have not been purchased by anyone throughout the year.

2. How is COGS Calculated?

Cost of Goods Sold depends on the change in inventory, which is computed by the LIFO, FIFO or weighted average methods. The COGS is then determined by a simple formula:

COGS = (Beginning inventory) + (Purchases during the period) – (Ending inventory)

Beginning inventory is the inventory at the end of the previous year and purchases during the year refers to any new stock that was acquired during the year. This gives us the total cost of all the inventory. But we want to calculate the cost of inventory sold during the period. Thus, we subtract the ending, or unsold, inventory from the total. Ending inventory is the inventory that remains, or is not sold by the end of the year.

3. Why is COGS Calculated?

Cost of Goods Sold is an important factor on which the gross profit of an enterprise depends. It is subtracted from the company’s revenues to obtain the net profit. Cost of Goods Sold is used as a parameter in calculating whether your company is charging a sufficient amount to its customers for its goods. The Gross Profit on the sale of a company’s goods must be sufficient to not only cover the cost of the goods, but also to cover the general and administrative operating costs of your company.

When it comes to recording your company’s expenses, it is important for you to not only have a handle on it operationally, but also to ensure that the financial statements prepared will address all the needs of your business. However, you need not be an expert in this. You can focus on your business and leave the stress of corporate accounting to chartered professional accountants. They are here to help you maintain timely and credible financial records.

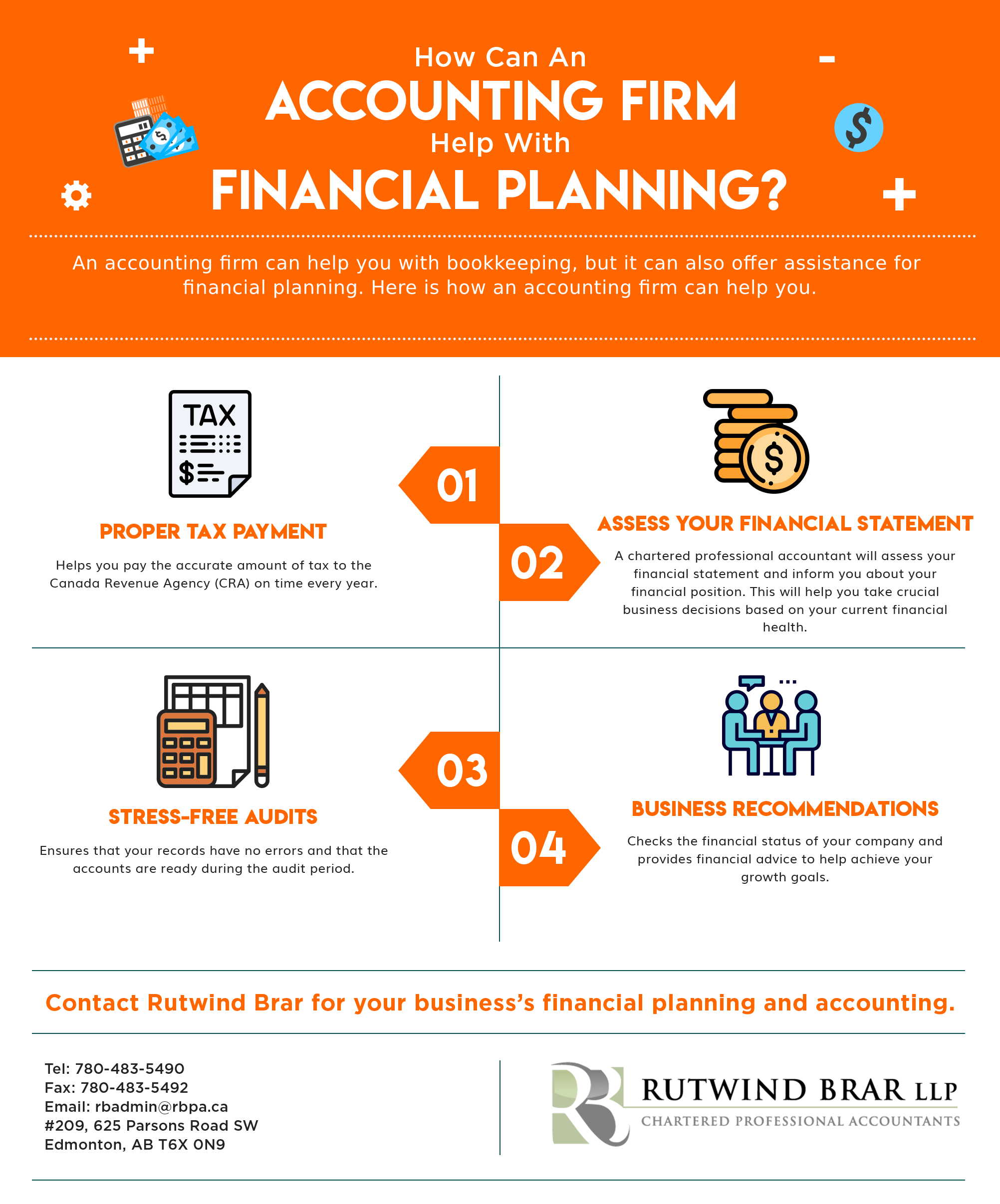

When you operate a business, financial planning is a process that needs extra attention. To provide this attention, you should consider employing an accounting firm to help you. An accounting firm performs several financial and bookkeeping tasks to help your business function smoothly. When you have an expert chartered professional accountant to look into your finances, the chances of discrepancies is reduced. Apart from reduced mistakes, here are some other aspects in which an accounting firm helps with financial planning.

Proper Tax Payment

Conducting your business operations within the tax laws and guidelines set by the government is crucial. A mistake often made by businesses is to not account for the tax amount to be paid to the Canada Revenue Agency (CRA). This happens when you are not aware of the percentage of tax levied on your services or products, or when your business does not have sufficient funds to pay the tax amount when its due. An accounting firm ensures that you are fully aware of the tax amount to be paid and helps you create a financial reserve for tax payment.

Financial Status and Health

As a business owner, it is vital that you keep an eye on the financial health of your business. This includes:

-

Income and Expenses

-

Profit and loss

-

Assets and liabilities

A chartered professional accountant will always be aware of your business’s financial health as they will regularly assess your financial statements. An accountant is well aware that knowing your business’s current financial health is vital if you wish to expand your business in the future.

Smooth Auditing Process

Audits are a time that any businessman dreads. The idea of an auditor going through your books of accounts and finding mistakes is scary. But what’s scarier is your inability to explain the reason for a mistake to the auditor. When you hire an accounting firm, the chartered professional accountant makes sure that your records have no mistakes and that the books are ready for an audit. Also, then you don’t end up with corporate accounting scandals!

Business Recommendations

The aim of growing your business can only be met if proper guidance is taken from experienced professionals. When an accounting firm is hired, it checks the complete financial state of the company and accordingly provides financial advice to overcome the shortcomings. Such accounting firms can also give you good advice about future investments based on your current financial state.

These are just some of the ways a chartered professional accountant can help you. If you are on the lookout for such services and more, reach out to the financial planning and accounting specialists in Edmonton.

As your business grows, the volume and the number of transactions increases. In such situations, entrepreneurs may find it difficult to focus on the core business activity and manage the books of account simultaneously. Therefore, you need an accountant to look after your accounts on a regular basis. Your business may require full-time bookkeeping services for multiple other reasons which are mentioned below.

Scarcity of Time

The more successful your business, the more time you dedicate to your business operations. As a result, you may not have sufficient time to maintain and record all your daily transactions. If you find yourself running short of time to maintain basic accounting entries, then it’s a sign you need to hire a full-time bookkeeper.

Irregular Bookkeeping

Bookkeeping is a time-consuming process, and it is extremely difficult to keep track of every transaction one makes. When you give the bookkeeping task to admin personnel, it can be quite challenging to juggle their daily operations along with regular bookkeeping. This leads to irregular bookkeeping. Irregular bookkeeping results in missing many financial records. Therefore irregularities in your accounts is a sign you need to consider hiring a professional bookkeeper.

Lack of Certainty

If there is lack of certainty about the accuracy of the records that you are keeping, this is another undeniable sign that the company is in desperate need of a bookkeeping service. In fact, certain mistakes can be very costly for your company. For example, if you do not enter some expenses which can be used to as a tax deduction, then you miss out on that tax deduction. As a result, you pay more tax than what you were supposed to.

Tax Filing Process is Complicated

It is crucial for a company to adhere to the latest regulations and laws that have been introduced. However, keeping up with these changes is difficult. When you are not aware of the exact tax rate that is applicable or the tax benefits for which your firm is eligible, the entire tax filing process can become complicated. Therefore, if you face difficulty in filing your tax returns every year, then you need to consider outsourcing your bookkeeping services to a professional accounting firm.

Setting up a department for bookkeeping is a tricky proposition since there is an additional cost of resources and workforce. It’s better to delegate these important responsibilities to firms that specialize in these tasks. You also make them accountable, and this leads to the reduced workload on your shoulders. Therefore, it’s recommended that you consult a bookkeeping services firm to manage all your accounting and bookkeeping operations on a regular basis.

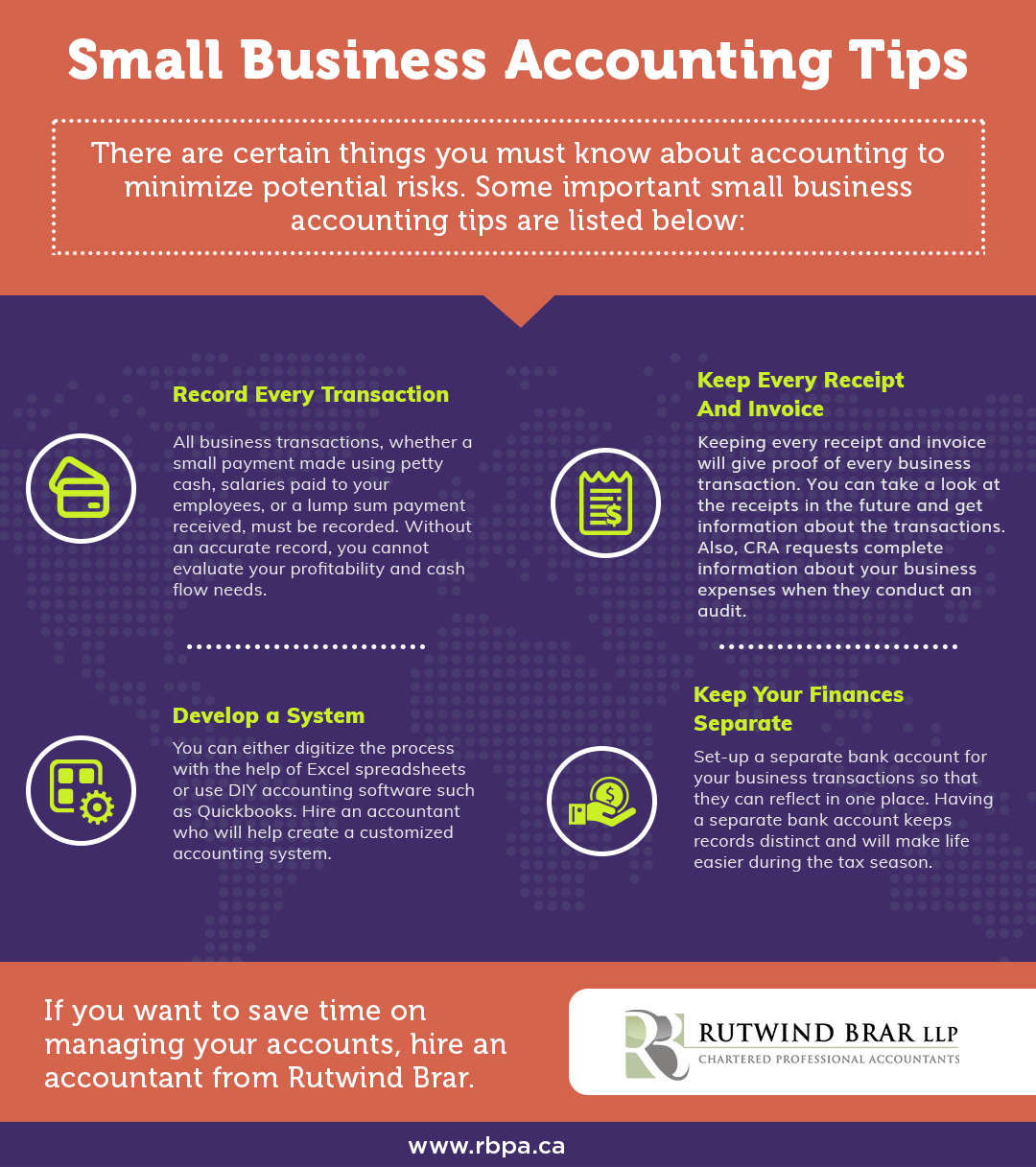

A business operates on capital and to keep a check on the income and expenses made in the business, regular and correct bookkeeping is crucial. Bookkeeping is the method of maintaining records of financial transactions taking place within a business. There are various ways in which bookkeeping can contribute towards a better functioning of your business. Here are some of the reasons why regular and timely bookkeeping is important for your business.

Easy Cash Flow Management

When running a business, keeping a check on your cash flow is essential. Issuing proper invoices to your customers and maintaining records on a daily basis is crucial. If the same is not followed, it leads to delays in receivables and payables, which could affect your cash flow adversely. Having a bookkeeping system ensures that proper entries are maintained thereby making it easy to know and manage your cash flow.

Helps in Tax Breaks

When your books of account are not maintained, you may miss out on transaction entries. Doing so will affect your tax planning. You may not realize this, but there are various expenses which are allowed as deductions according to the Income Tax Act and expenditures which are not fully deductible for income tax purposes.Accurate recording of transactions will ensure that expenditures are recorded in order to be able to give them the proper tax treatment at your company’s fiscal year-end.

Aids Future Planning

Often business owners assume they are making a profit without proper bookkeeping and just by taking the incoming money to be profit. This is a mistake and can be avoided by correct bookkeeping. When you have a detailed record of your expenses and incomes, it becomes easier to make informed decisions about your business’s future. The main bookkeeping statements you need to check are the balance sheet and the profit and loss statements to get a complete insight into your current standing and financial health.

Easy Presentation to Investors

The first thing that an investor may ask for before investing money in your business is to have a look at not only your company’s prior Year End Financial Statements and Corporate Income Tax Returns, but also your bookkeeping for the current year. Having a disheveled bookkeeping will give an impression to the investor that you are not a focused business owner. When your bookkeeping is accurate and well kept, it becomes easier to provide reports of financial growth and profitability to the investor.

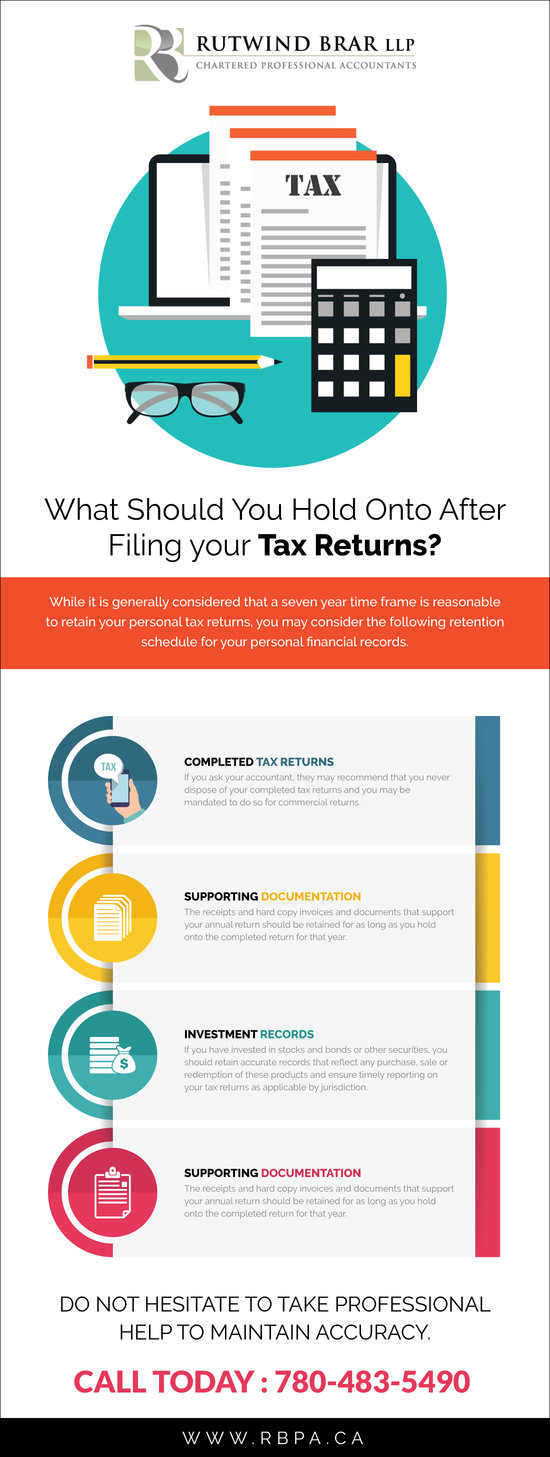

Do not hesitate to take professional help to maintain accuracy. Reach out to one of the finest chartered accounting firms for comprehensive consultation on your bookkeeping.

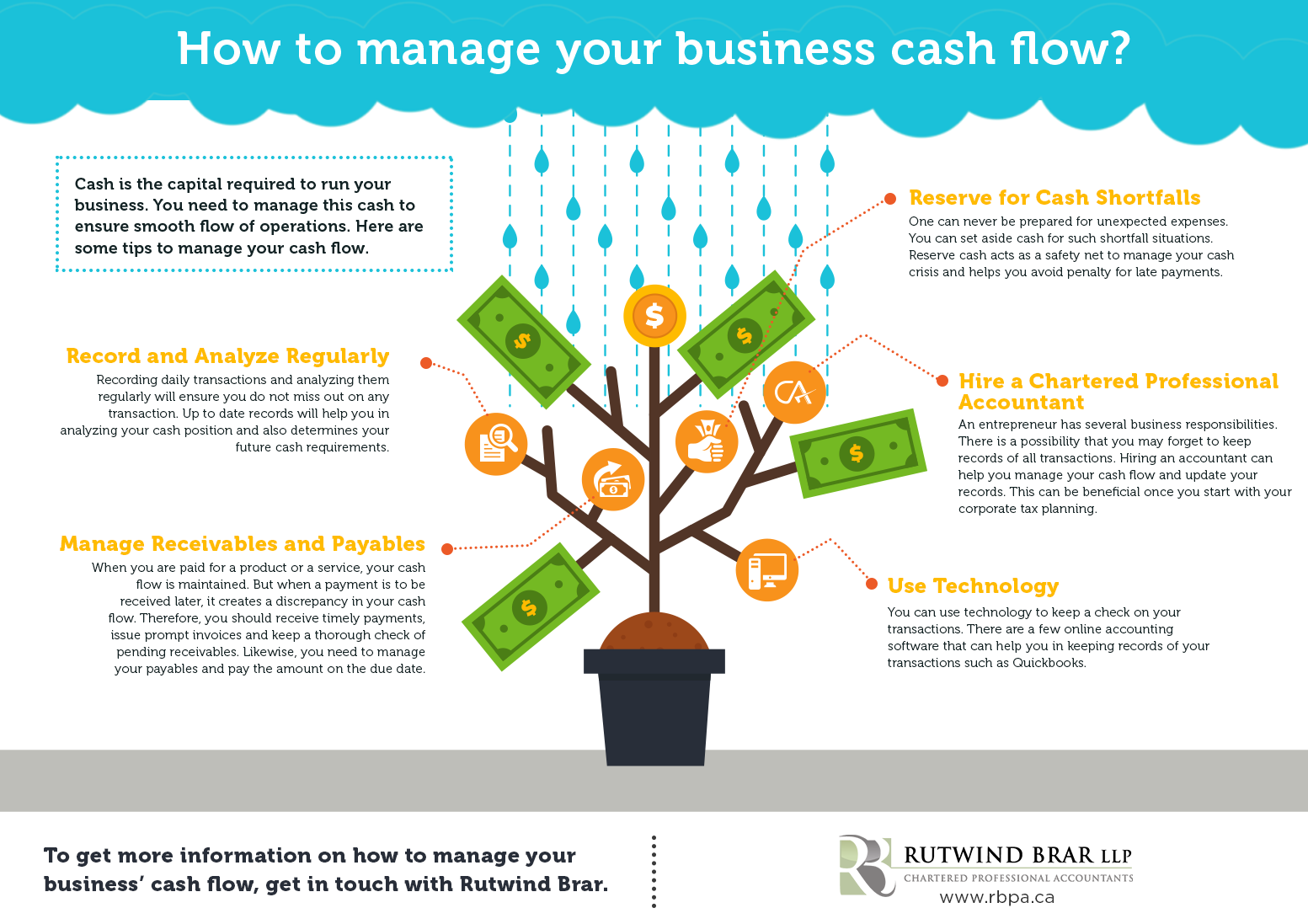

Cash flow refers to the movement of cash in and out of a business. It is the capital required to run your business on a daily basis. For a smooth functioning of the daily operations, it is essential to manage your cash flow. Consider the following tips to manage your business cash flow suggested by chartered professional accountants.

Record and Analyze Regularly

The very first step in proper cash flow management is the recording of every transaction being made in the business on a regular basis as this will avoid the chances of missing out on any transaction. Up to date records will allow you to analyze your cash position and determine your future cash requirements. You will therefore be well-prepared with sufficient cash as and when payments for expenses are due.

Manage Receivables and Payables

The two major factors which affect your cash flow significantly are your receivables and payables. When you are paid for a product or service immediately, your cash flow is maintained. However, if the payment is to be received later, it creates a discrepancy in your cash flow. To make sure your cash flow is not affected ensure that you get timely payments, issue prompt invoices and keep a thorough check of pending receivables. Similarly, when managing your payables, make complete use of the credit period. For instance, don’t make a payment in 15 days if it due after 30 days unless you are offered any discount for early payment.

Reserve for Cash Shortfalls

You can never be fully prepared for any unexpected expenses. For situations like these, having a reserve of cash set aside for such shortfalls is a must. Having a reserve of cash acts as a safety net to manage your cash crisis and avoid attracting any penalty for late payments in the form of interest.

Hire a Chartered Professional Accountant

As an entrepreneur, there are various aspects of business you need to look into. With too many business responsibilities, you may end up not maintaining records of your transactions on a daily basis. This leads to discrepancies in the future. Therefore, it’s recommended that you take professional help. Having an accountant to look after your daily transactions will not only allow you to manage your cash flow but also have an updated accounts statement. This can be very beneficial once you start with your corporate tax planning.

Use Technology

Another easy and error-free method to manage your cash flow is to make use of technology. You can make use of online accounting software such as QuickBooks to maintain your records and also look after invoices and payments. There are various types of software available for this accounting purpose. Choose a software as per your need.

There are many more methods to manage cash flow in a better way which chartered professional accountants can help you with. Offering discounts to debtors, raising invoices on time, informing debtors before the due date, etc. are some ways to ensure your payments are on time and you do not face the problem of cash shortage. To get more information about how to manage your business cash flows, get in touch with the best chartered professional accountants and experts.